Key Changes in Tax Audit Regulations Effective FY 2026-27

6/28/20251 min read

Key Changes Effective FY 2026‑27 (from April 1, 2026)

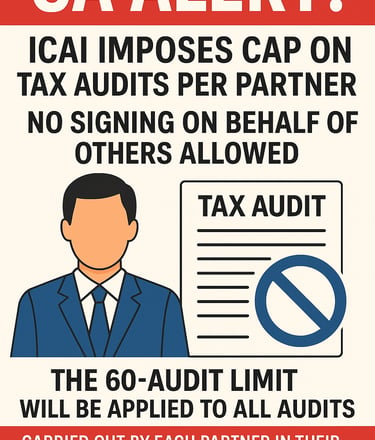

Each partner is limited to a maximum of 60 tax audits per year, whether undertaken individually or as part of a firm.

No proxy signing allowed—a partner cannot sign reports on behalf of another under any circumstances .

Applies across all firms, so even if a CA is a partner in multiple entities, the cap is aggregate

Backed by UDIN oversight to strengthen accountability and curb forged or excessive signings

🎯 Objectives & Implications

Improve audit quality and transparency by reducing over-concentration of audits with senior partners.

Promote equitable delegation—firms must distribute assignments across partners and possibly onboard more partners.

Encourage structural adjustments, training of junior partners, and the adoption of audit management tools .

🛠 Bottom Line for Firms & CAs

Implement tracking systems to monitor audit counts per partner (including via UDIN).

Restructure partner workloads—ensure no one exceeds 60 in aggregate.

Hire or elevate partners to manage client needs without overload.

Train partners thoroughly to handle audit signings responsibly and comply with ethics.