Understanding ITR Filing Requirements for Foreign Income, Shares, ESOPs, and Assets in India

6/19/20251 min read

Introduction to ITR Filing and its Importance

Income Tax Return (ITR) filing in India is an essential process that enables individuals to report their income to the Income Tax Department. This reporting is not just a legal obligation but also serves as a crucial tool for taxpayers to maintain compliance with the Indian Income Tax Act. The act governs the taxation framework across various income classes and categories, ensuring that all taxpayers contribute fairly to the nation's revenue. Failing to comply can result in penalties and legal repercussions, making it vital for everyone to understand the specifics of ITR filing.

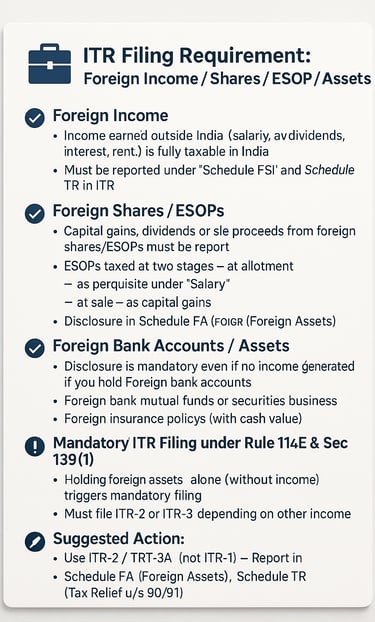

💼 ITR Filing Requirement: Foreign Income / Shares / ESOP / Assets

If you are a Resident and Ordinarily Resident (ROR) in India, you must file ITR if you have any of the following during the financial year:

✅ 1. Foreign Income

Income earned outside India (salary, dividends, interest, rent, etc.) is fully taxable in India for RORs.

Must be reported under "Schedule FSI" and "Schedule TR" in ITR.

✅ 2. Foreign Shares / ESOPs

Capital gains, dividends, or sale proceeds from foreign shares/ESOPs must be reported.

ESOPs taxed at two stages:

At allotment – as perquisite under “Salary”

At sale – as capital gains

Disclosure in Schedule FA (Foreign Assets).

✅ 3. Foreign Bank Accounts / Assets

Even if no income is generated, disclosure is mandatory if you hold:

Foreign bank accounts

Foreign mutual funds or securities

Foreign real estate or business

Foreign insurance policies (with cash value)

✅ 4. Mandatory ITR Filing under Rule 114E & Sec 139(1)

Holding foreign assets alone (without income) triggers mandatory filing.

You must file ITR-2 or ITR-3 depending on your other income.

Not filing can result in penalty & prosecution under Black Money Act.

⚠️ Note:

NRI or RNOR? You are not required to disclose or pay tax on foreign income/assets unless earned or received in India.

Proper valuation & disclosure as per CBDT guidelines is crucial.

📌 Suggested Action:

Use ITR-2 / ITR-3 (not ITR-1)

Report in:

Schedule FA (Foreign Assets)

Schedule FSI (Foreign Source Income)

Schedule TR (Tax Relief u/s 90/91)